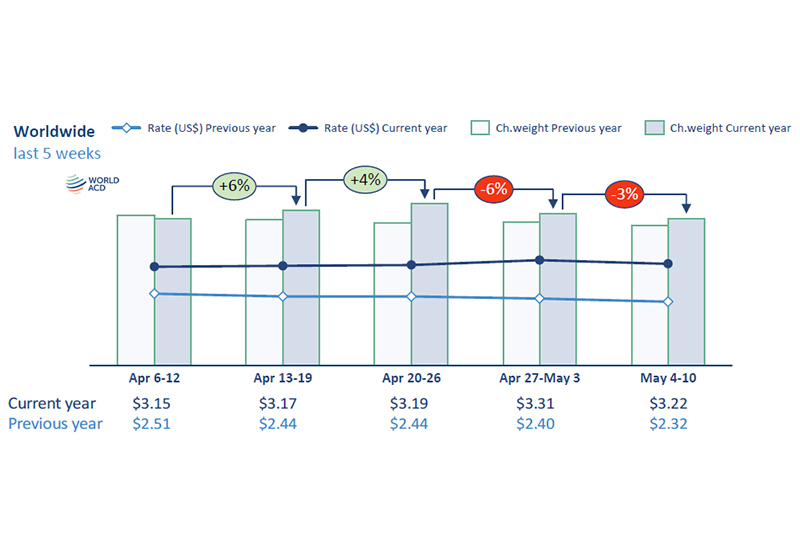

In the first full week of May airfreight retreated on a global basis from the previous week (WoW) both in terms of chargeable weight and pricing, accompanied by a reduction in capacity. This was driven by the conclusion of the holiday period in Asia and the end of the boom in flower traffic for Mother’s Day. On an annual basis traffic as well as pricing remained elevated.

Global tonnage shrank -3% WoW to a combined -6% drop for weeks 18 and 19 from the previous fortnight (2Wo2W), based on the more than 500,000 weekly transactions covered by WorldACD’s data. A major reason for the decline was the end of the Mother’s Day flower surge, which reduced volumes especially out of Central and South America (CSA) by -19% WoW and by -9% 2Wo2W. Chargeable weight out of Asia Pacific dropped -5% WoW and -8% 2Wo2W respectively as the Super Golden Week holiday ended. Tonnage out of the Middle East & South Asia (MESA) region also declined (-4% WoW), whereas traffic from North America and Europe climbed +5% and +2% WoW respectively, driven by rebounding demand from Asia post holiday period. On an annual basis (YoY) global tonnage was up +5%, with single-digit increases from all origins except Africa (-11%).

The Super Golden Week holiday (packing Japan’s Golden Week alongside public holidays in China and South Korea) reduced outbound volumes from Asia Pacific by -9% WoW both to Europe and USA, with chargeable weight outbound Japan dropping -44% to USA and -54% to Europe. While volumes from Asia Pacific to USA fell WoW in all sectors, chargeable weight from Vietnam to Europe jumped +22%. Airborne exports to other European destinations declined, except from Thailand (0%) and Taiwan (+1%)

Volume from MESA dropped -5% WoW both to USA and Europe, but the underlying dynamics were starkly different. Traffic to Europe declined owing to double-digit drops out of Dubai and Bangladesh, whereas chargeable weight to USA jumped +65% from Dubai (following a double-digit drop the previous week), but was hit by declines of -7% out of India and -5% from Sri Lanka. On an annual basis, chargeable weight from MESA was up +11% to USA but down -1% to Europe, resulting in a +6% gain overall for MESA origin airfreight.

Chargeable weight from Asia Pacific to Europe slipped -1% YoY due to falling tonnage out of Japan, Indonesia and Hong Kong, while exports from the region to USA were up +33%, with chargeable weight increasing out of all origins except Indonesia (-21%) and Japan (-2%). Volumes out of China and Hong Kong to USA climbed almost +50%.

Faced with slower demand, global pricing retreated -3% WoW to an average rate of US$3.22, matching the percentage drop in global chargeable weight. With the exceptions of Europe (+1%) and North America (flat), rates dropped in single digits in all markets, led by declines of -8% from CSA and -7% from Africa, largely a reflection of the end of Mother’s Day flower traffic. On an annual basis, CSA was the only origin region showing single digit YoY rate growth (+7%), while elsewhere pricing jumped between +22% (North America) and +56% (MESA). Overall pricing was +39% up YoY, with spot prices +51% higher.

Week on week spot rates from MESA dropped -3% to Europe, retreating in low single digits in all origins except Dubai (+7%). Single digit declines out of all MESA origins added up to a collective -3% WoW drop in pricing to USA. On an annual basis, spot rates from MESA to USA were up +60%, with double-digit increases out of all markets topped by a +135% jump from Dubai, which also led price increases to Europe (+72% from MESA overall) with a +181% jump.

The end of the flower rush and Super Golden Week ushered in a decline of capacity, which fell globally -2% WoW, following flat momentum in week 18. It dropped -4% in CSA, -3% from Asia Pacific and -2% both out of North America and Africa. Growth from Europe and MESA was flat, an indication that the rebuild of capacity in the latter area is losing momentum. Freighter operations by Gulf-based carriers have been largely restored, but the full recovery of passenger operations is not expected before a lasting end of the conflict has been reached and travelers feel confident to fly to the region again.

Soaring fuel costs cause airlines to reduce or scrap unprofitable sectors. For the most part these are regional routes served with narrowbody aircraft, so the impact on cargo capacity has been negligible, but some long-haul sectors have been affected. Airlines have cut altogether 13,000 flights in May, and industry observers expect more changes to passenger schedules as aviation fuel prices are not likely to drop significantly in the near future. So far the situation does not appear to have slowed travel demand, but the elevated cost of flying may push consumers to change their vacation plans, triggering further airline schedule reductions.